BCom 2nd Semester Business Economics Solved Question Paper 2024")

Gauhati University (GU) BCom 2nd Semester Business Economics Solved Question Paper 2024

1 (Sem-2) MDC 09

2024

MULTI DISCIPLINARY COURSE

Paper Code: MDC0200903

(Business Economics)

Full Marks: 45

Time: 2 hours

The figures in the margin indicate full marks for the questions

1. Choose the correct answer of the following: 1×5=5

(a) Which of the following is not a part of microeconomics?

(i) Factor pricing

(ii) National income

(iii) Demand analysis

(iv) Market analysis

Answer: (ii) National income

Explanation: National income is a concept studied under macroeconomics, as it deals with the overall economy's income and production.

(b) An inferior good is a commodity whose with an increase in income.

(i) demand falls

(ii) demand rises

(iii) supply falls

(iv) supply rises

Answer: (i) demand falls

Explanation: Inferior goods experience a decrease in demand as consumers' income rises, as they tend to shift to superior alternatives.

(c) The shape of the TFC curve is

(i) U-shaped

(ii) rectangular hyperbola

(iii) straight line parallel to X-axis

(iv) straight line parallel to Y-axis

Answer: (iii) straight line parallel to X-axis

Explanation: TFC remains constant irrespective of the level of output, so its curve is a horizontal line parallel to the X-axis.

(d) Which of the following can be used to control credit creation in the economy?

(i) Bank Rate

(ii) Statutory Liquidity Ratio

(iii) Both (i) and (ii)

(iv) None of the above

Answer: (iii) Both (i) and (ii)

Explanation: The Bank Rate and Statutory Liquidity Ratio (SLR) are monetary tools used by the central bank to regulate credit creation by influencing the cost and availability of credit.

(e) Which of the following is an example of market form where the firms are price- makers?

(i) Perfect competition

(ii) Monopoly

(iii) Oligopoly

(iv) Monopolistic competition

(e) Which of the following is an example of a market form where the firms are price-makers?

Answer: (ii) Monopoly

Explanation: In a monopoly, a single firm dominates the market and has significant control over the price of its product, making it a price-maker. Other market forms involve price-taking to varying extents due to competition.

2. Answer the following questions (any five): 2×5=10

(a) State the use of economics in business.

Answer:

1. Helps in deciding prices for products and services.

2. Guides in planning production to meet demand.

3. Assists in understanding customer needs and preferences.

4. Helps in using resources effectively to increase profit.

(b) Define an oligopoly form of market.

Answer:

An oligopoly is a market where only a few companies control most of the business. These companies influence prices and are affected by what their competitors do.

(c) "Change in demand and change in quantity demanded are the same." Comment.

Answer:

This statement is wrong. Change in demand means the whole demand curve shifts because of factors like income or preferences. Change in quantity demanded happens when the price of the product changes, moving along the same demand curve.

(d) State any two exceptions to the law of demand.

Answer:

1. Giffen Goods: When the price of certain low-quality goods increases, people may still buy more of them.

2. Luxury Goods: Expensive items like jewelry or branded products may have higher demand when their price increases because people see them as status symbols.

(e) Mention any two advantages of demand forecasting.

Answer:

1.Better Planning: It helps businesses decide how much to produce and store.

2.Less Risk: It reduces the chances of having too much or too little stock.

(f) Define money supply.

Answer: Money supply is the total money available in a country, including cash and money in bank accounts.

(g) How does an increase in GDP help in capital formation?

Answer: When GDP grows, people earn more money. This leads to more savings and investments, which helps build things like factories, roads, and machines.

(h) If X and Y are complementary goods, how does a rise in the price of Y affect the demand for X?

Answer:

If the price of Y goes up, fewer people will buy it. Since X is used with Y, the demand for X will also go down.

(i) Differentiate between long-run production and short-run production.

Answer:

1. Short-Run Production: Some resources, like machines, are fixed, while others, like workers, can change.

2. Long-Run Production: All resources can change, so companies can fully adjust to changes in demand.

(j) Define 'constant returns to scale.'

Answer: Constant returns to scale mean that if you double the inputs (like labor and materials), the output will also double. This shows that efficiency stays the same.

3. Answer the following questions (any four):5×4=20

(a) Describe the features of monopoly.

(b) Explain the procedure of price determi- nation under perfect competition.

(c) Discuss the various properties of an isoquant.

(d) A consumer spends 1,000 on a good at a price of 10. When its price falls by 20%, he spends 800. Calculate elasticity of demand (ED) using percentage method.

(a) Describe the features of monopoly.

Answer:

1. Single Seller: A monopoly has only one seller or producer in the market.

2. No Close Substitutes: The product has no close substitutes, making it unique.

3. Price Maker: The monopolist decides the price of the product.

4. High Barriers to Entry: New firms cannot easily enter the market due to legal, financial, or technical restrictions.

5. Lack of Competition: There is no competition in the market.

(b) Explain the procedure of price determination under perfect competition.

Answer:

1. Market Equilibrium: Price is determined where market demand equals market supply.

2. Perfect Knowledge: Buyers and sellers have complete knowledge about prices and products.

3. No Influence on Price: Individual buyers and sellers cannot influence the market price; they are price takers.

4. Free Entry and Exit: Firms can freely enter or leave the market based on profit opportunities.

5. Uniform Price: All firms sell their products at the same price.

(c) Discuss the various properties of an isoquant.

Answer:

1. Downward Sloping: Isoquants slope downward from left to right, showing that less of one input is used if more of another input is used to maintain the same output.

2. Convex to the Origin: Isoquants are convex, indicating diminishing marginal rate of technical substitution (MRTS).

3. Do Not Intersect: Isoquants do not cross each other, as each represents a specific level of output.

4. Higher Isoquants Represent More Output: An isoquant further from the origin shows a higher level of production.

5. Elasticity of Substitution: Shows how easily one input can be substituted for another.

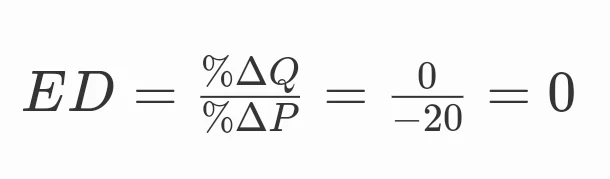

(d) A consumer spends 1,000 on a good at a price of 10. When its price falls by 20%, he spends 800. Calculate elasticity of demand (ED) using the percentage method.

Answer:

1. Initial Price (P1): ₹10

2. New Price (P2): ₹10 - (20% of ₹10) = ₹8

3. Initial Quantity (Q1): ₹1,000 / ₹10 = 100 units

4. New Quantity (Q2): ₹800 / ₹8 = 100 units

5. Percentage Change in Quantity:

(e) Explain the various types of price elasticity of demand.

Answer:

1. Perfectly Elastic Demand (ED = ∞): Even a small change in price causes an infinite change in quantity demanded.

2. Perfectly Inelastic Demand (ED = 0): Quantity demanded remains unchanged regardless of price changes.

3. Unitary Elastic Demand (ED = 1): A percentage change in price leads to an equal percentage change in quantity demanded.

4. Elastic Demand (ED > 1): A small percentage change in price leads to a larger percentage change in quantity demanded.

5. Inelastic Demand (ED < 1): A percentage change in price causes a smaller percentage change in quantity demanded.

(f) Describe the various tools used for monetary policy in India.

Answer:

1. Repo Rate: The interest rate at which the Reserve Bank of India (RBI) lends money to banks.

2. Reverse Repo Rate: The interest rate at which banks deposit money with the RBI.

3. Cash Reserve Ratio (CRR): The percentage of total deposits that banks must keep as reserves with the RBI.

4. Statutory Liquidity Ratio (SLR): The percentage of net demand and time liabilities banks must keep in government-approved securities.

5. Open Market Operations (OMO): Buying and selling of government securities by the RBI to control liquidity.

6. Bank Rate: The rate at which the RBI lends to commercial banks without securities.

7. Monetary Policy Instruments: Quantitative and qualitative measures to control credit and money supply.

(g) Discuss the shape of the MC curve with reference to the MP curve by showing the relationship between them.

Answer:

1. Marginal Product (MP) Curve: The MP curve shows the additional output produced by one extra unit of input. It initially rises, reaches a maximum, and then declines due to the law of diminishing returns.

2. Marginal Cost (MC) Curve: The MC curve represents the additional cost incurred in producing one more unit of output.

3. Relationship:

When the MP curve is rising, the MC curve is falling.

When the MP curve is at its maximum, the MC curve is at its minimum.

When the MP curve starts falling, the MC curve starts rising.

Conclusion: The MC and MP curves are inversely related.

(h) Elucidate the various characteristics of business economics.

Answer:

1. Applied Economics: It applies economic theories to solve real-world business problems.

2. Microeconomic in Nature: Focuses on individual firms and industries.

3. Decision-Oriented: Helps in making decisions about pricing, production, and cost management.

4. Interdisciplinary: Combines economics with finance, management, and accounting.

5. Future-Oriented: Involves forecasting and planning to deal with uncertainty in business.

6. Practical Approach: Aims to provide solutions that are useful for business management.

4. Answer the following questions (any one): 10

(a) Explain producer's equilibrium through the use of isoquants and isocosts.

Answer: Producer's equilibrium happens when a firm chooses the best combination of inputs (like labor and capital) to produce the most output at the lowest cost.

Isoquants:

An isoquant is like a curve that shows all the different combinations of two inputs (labor and capital) that will give the same amount of output.

It’s similar to how an indifference curve works for consumers, but for producers.

The curve slopes down because adding more of one input (like labor) while reducing the other (like capital) keeps the output constant, but with less efficiency over time.

Isocosts:

An isocost line shows all the combinations of labor and capital that a firm can buy for the same total cost.

The slope of the isocost line depends on the prices of labor and capital. If labor is cheap compared to capital, the firm might use more labor and less capital.

Producer's Equilibrium:

The producer’s equilibrium is found when the isoquant touches the isocost line at a single point.

At this point, the firm is getting the best use of its resources, because the rate at which the firm is willing to trade one input for another (called MRTS) is equal to the rate at which the market allows them to trade (based on the prices of labor and capital).

This means the firm has found the cheapest way to produce the most output.

In simple terms, producer's equilibrium is when a firm uses its resources in the best possible way to get the highest output for the lowest cost. This happens where the isoquant and isocost line meet.

(b) State and explain the law of demand.

Answer:

Law of Demand:

The law of demand states that, ceteris paribus (all other things being equal), when the price of a good or service decreases, the quantity demanded of that good or service increases, and vice versa. This implies an inverse relationship between price and quantity demanded.

Explanation:

The law of demand can be explained as follows:

Inverse Relationship: There is a negative relationship between price and quantity demanded. When the price of a product rises, consumers tend to buy less of it. Conversely, when the price falls, they tend to buy more.

Reason for the Inverse Relationship:

Income Effect: When the price of a good decreases, consumers feel as if their purchasing power has increased, allowing them to buy more of the product.

Substitution Effect: When the price of a good decreases, it becomes relatively cheaper than its substitutes, encouraging consumers to buy more of it instead of alternatives.

Assumptions of the Law of Demand:

There are no changes in consumer income.

Consumer preferences remain constant.

Prices of related goods (substitutes and complements) do not change.

There is no expectation of future price changes.

Diagrammatic Representation:

The demand curve is typically downward-sloping from left to right, indicating the inverse relationship between price and quantity demanded.

Exceptions to the Law of Demand:

There are some cases where the law of demand may not hold true, such as:

Giffen Goods: Inferior goods for which demand increases as the price rises due to the strong income effect.

Veblen Goods: Luxury goods for which higher prices increase their desirability as a status symbol.

Necessities: Essential goods may not follow the law of demand strictly because their demand is less sensitive to price changes.

In conclusion, the law of demand highlights the fundamental economic behavior of consumers, showing how price influences the quantity demanded in the market.

(c) Explain 'total expenditure method' and 'geometric method' of measuring price elasticity of demand. 5+5=10

Answer:

Total Expenditure Method and Geometric Method of Measuring Price Elasticity of Demand

Total Expenditure Method (5 Marks)

The Total Expenditure Method measures price elasticity of demand by analyzing the relationship between changes in price and total expenditure (or total revenue) on a good.

Total Expenditure = Price × Quantity Demanded

Steps to Measure Elasticity:

Elastic Demand (Ed > 1):

If the price falls and total expenditure increases, or if the price rises and total expenditure decreases, demand is elastic.

(Consumers respond strongly to price changes.)Inelastic Demand (Ed < 1):

If the price falls and total expenditure decreases, or if the price rises and total expenditure increases, demand is inelastic.

(Consumers do not change how much they buy significantly.)Unitary Elastic Demand (Ed = 1):

If the price changes but total expenditure stays the same, demand is unitary elastic.

Example:

Suppose the price of a product falls from ₹10 to ₹8:

Quantity demanded increases from 100 units to 150 units.

TE at ₹10 = ₹10 × 100 = ₹1,000

TE at ₹8 = ₹8 × 150 = ₹1,200

Since total expenditure increased, the demand is elastic (Ed > 1).

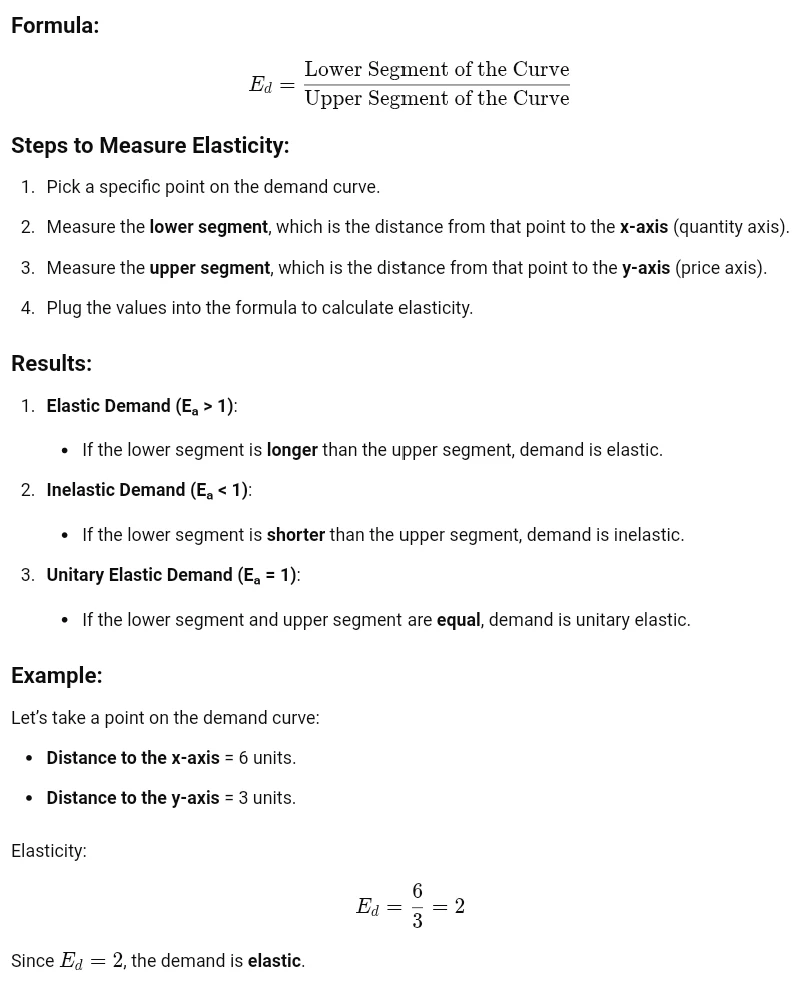

Geometric Method (5 Marks)

The Geometric Method (also called the Point Method) helps calculate the price elasticity of demand at a specific point on the demand curve.

(d) Define perfect competition. Explain the characteristics of perfect competition. Give any, one example that is close to perfect competition in the real world. 2+7+1=10

Answer: Definition of Perfect Competition: Perfect competition is a market structure where a large number of buyers and sellers trade a homogeneous product, and no individual can influence the market price. The market price is determined by the forces of demand and supply.

Characteristics of Perfect Competition

Large Number of Buyers and Sellers

There are so many buyers and sellers that no single one can influence the market price. Sellers act as price takers.

Homogeneous Product

All sellers sell identical or similar products, so consumers don’t differentiate between products from different sellers.

Free Entry and Exit

Firms can enter or leave the market freely without facing any major barriers like high costs or legal restrictions.

Perfect Knowledge

Buyers and sellers have complete knowledge of the market conditions, including prices, products, and competition.

No Control Over Prices

Since products are identical, no seller can charge more than the market price, and buyers won’t pay more than necessary.

Perfect Mobility of Resources

Factors of production like labor and capital can move freely in and out of the industry.

No Government Intervention

There is no interference from the government in terms of taxes, subsidies, or price controls.

Absence of Transportation Costs

Transportation costs are assumed to be zero or negligible, ensuring uniform prices across the market.

Example of a Market Close to Perfect Competition The agricultural market is an example close to perfect competition. For instance, the wheat market has many buyers and sellers, and wheat is a homogeneous product. Farmers cannot influence the price and must accept the market price.

-00000-

![Business Economics Solved Question Paper 2024 [Gauhati University BCom 2nd Semester NEP FYUGP]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEh5BGZuLJa2DfSX9Lmf9VUFZsuRRKFW1PGM6Hglbb6vg9_K-9DRgsRzsoMlA1TFsomk1LUyd_9xIx-GR1-Pm3ajTiO6qJ-4mw91sL1rN5XtYvNZdD1R7DXkEQ__ML2bl0yUUcm73L5YWiMzAiBb_9jnfi8YiHwayoaeqsX44Q92G2jC49MZhr_WYOMwHwkk/w200-h200-p-k-no-nu/Business%20Economics%20Solved%20paper%202024.jpg)