![Auditing Solved Question Paper 2023 [Dibrugarh University BCom 6th Semester]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjQB6Whgd-k11pOx4CaoSjAQXWPVCZMwqiOniD3mu2DlmfhO_OU7MBZ-07UV_2lfB-cX05thmiJQzXduq3g1kOm42Qm2N4a-mM2fC9ihP4WBxRFQKaoD7_w-dhq0U4DpgguB_V91IAE8jCfEYnMBN1TMoCdgwZv7CgEobDbVUPJbKjAS4yABxtubrFcMyLC/s1120/Dibrugarh%20auditing%20solve%20question%20paper%202023.jpg "Dibrugarh University BCom 6th Semester Auditing Solved Question Paper 2023")

Dibrugarh University: Auditing Solved Question Paper 2023

[Dibrugarh University BCOM 6th Semester]

Auditing Solved Question Paper 2023

COMMERCE (Core)

Paper: C-603

(Auditing)

Full Marks: 80

Pass Marks: 32

Time: 3 hours

The figures in the margin indicate full marks for the questions.

1. (a) State whether the following statements are True or False: 1 x 4 = 4

(1) Auditing starts where accounting ends.

ANS:- True

(2) Patents must be valued at cost less depreciation.

ANS:- False

(3) An auditor is not liable to third parties.

ANS:- False

(4) U/S 129(2), the auditor’s report is attached to every financial statement.

ANS:- True

(b) Fill in the blanks with appropriate word(s): 1x4=4

(1) When an audit is conducted without any legal necessity, the audit is called Non-Statutory Audit

(2) When written evidence is available in original, it is known as Primary voucher.

(3) Share Premium Account may be used for issuing bonus shares or writing off preliminary expenses.

(4) Audit report with reservation is known as Qualified Audit Report.

2. Write short notes on any four of the following: 4 x 4 = 16

(a) Errors of omission.

Ans:- Errors of omission are essentially failures to take required actions, complete tasks, or provide necessary information. These omissions occur when someone neglects to do something that they should have done. This can be happen due to oversight, forgetfulness, or lack of knowledge. In various fields:

1. Financial Accounting: Omission errors might occur in financial reports when a company fails to record a transaction or an important piece of information, leading to inaccurate financial statements.

2. Medicine and Healthcare: Medical errors of omission involve failing to administer proper treatment, prescribe necessary medication, or provide essential information to patients, impacting their care and well-being.

3. Legal Context: Errors of omission in legal documents or contracts can result in incomplete agreements, missing clauses, or overlooked terms that could lead to disputes or legal complications.

4. Project Management: Failing to include essential tasks, steps, or milestones in a project plan represents errors of omission, potentially causing delays or inefficiencies in completing the project.

Addressing errors of omission often involves thorough review, adherence to checklists or procedures, and fostering a culture of attention to detail to prevent these oversights and ensure completeness in various processes and endeavors.

(b) Verification of contingent liabilities.

Ans: Verification of contingent liabilities involves assessing the likelihood and potential impact of future events that may create obligations for a company.

The following are the brief overview o contingent liabilities:

1. Identification: Contingent liabilities are potential obligations arising from past events. They may include legal disputes, product warranties, or guarantees.

2. Assessment: The company evaluates the likelihood of these contingencies becoming actual liabilities. Factors such as legal advice, historical data, and industry norms are considered.

3. Measurement: If the likelihood of a contingent liability is probable and the amount can be reasonably estimated, it is recorded in the financial statements. Otherwise, it is disclosed in the footnotes.

4. Disclosure: Even if a contingent liability is not recorded, it must be disclosed in the footnotes of the financial statements along with relevant details such as nature, potential impact, and management's assessment.

5. Review: Contingent liabilities are regularly reviewed and reassessed. Changes in circumstances or new information may alter their classification or measurement.

Verification ensures that contingent liabilities are properly recognized, measured, and disclosed in the financial statements, providing transparency and reliability to stakeholders.

(c) Audit of forfeiture of shares.

Ans: The audit of forfeiture of shares involves a thorough examination to ensure that the forfeiture process complies with the legal framework and the company’s articles of association. When a shareholder fails to pay the call on shares or instalments of the issue price within the specified time, the company may forfeit their shares.

The auditor’s role is to verify that:

1. Provisions for Forfeiture: The auditor checks the company's articles to confirm that they authorize the board of directors to forfeit shares.

2. Resolution and Notice: They ensure that a proper resolution was passed by the board and that the shareholder was given due notice of the forfeiture.

3. Contractual Obligations: The auditor examines if the forfeiture aligns with the contractual obligations between the shareholder and the company.

4. Accounting Treatment: They review the accounting entries related to the forfeiture to ensure that they accurately reflect the reversal of share issue entries and adjustments to capital accounts.

The audit ensures that the forfeiture process is carried out fairly and in accordance with the company's regulations, protecting the interests of both the company and its shareholders. It also involves checking that the company has maintained proper records and documentation of the forfeiture process.

(d) Government audit.

Ans:

Government Audit: Ensuring Public Trust and Accountability

A government audit is a critical tool for maintaining public trust in the financial integrity of government institutions. It involves a systematic review of various aspects of government operations, including financial records, compliance with laws and policies, and the efficiency and effectiveness of programs and services.

The audit is typically conducted by an independent and objective body, such as the Comptroller and Auditor General (CAG) in India, which has the authority to examine the use of public funds by government entities. The process includes evaluating whether resources are being used economically and whether government activities are achieving their intended results.

The outcomes of a government audit can lead to recommendations for improvements, identification of areas where resources can be better utilized, and, in some cases, the detection of mismanagement or fraud. By providing this oversight, government audits play a vital role in ensuring that public entities operate in the best interest of the citizens they serve.

In essence, government audits are a cornerstone of good governance, helping to ensure that governments operate with integrity, efficiency, and in compliance with the law.

(e) Importance of audit report.

Ans: The audit report is a crucial document that represents the culmination of the audit process. It contains the auditor's formal opinion on the accuracy and reliability of an organization's financial statements. Here's a short note on its importance:

An audit report is important for several reasons:

- Assurance: It provides stakeholders with assurance that the financial statements are free from material misstatement and are in compliance with accounting standards.

- Credibility: A clean audit report enhances the credibility of the financial information, which is essential for investors, creditors, and the market.

- Decision Making: It aids in informed decision-making by providing a reliable basis for evaluating the financial health and performance of an organization.

- Compliance: The report indicates whether the company is adhering to legal requirements and financial regulations.

- Confidence: For the management and shareholders, it serves as a testament to the company's integrity and effective governance.

In essence, the audit report plays a important role in establishing trust between the organization and its stakeholders, ensuring that the financial statements can be relied upon for accuracy and transparency.

3. (a) What do you mean by auditing? Discuss the basic principles while conducting an audit. 4+10=14

Ans: Auditing is a systematic examination of the books and records of a business or other organization, in order to ascertain or verify and report upon the facts regarding its financial operation and the result thereof.

The following are the basic principles while conducting an audit:

1. Integrity: Auditors must be honest, objective, and unbiased in their work, maintaining integrity and professional skepticism throughout the audit process.

2. Objectivity: Auditors need to remain impartial and independent from the entity being audited, ensuring their judgment is not influenced by personal or external factors.

3. Confidentiality: Auditors must respect and protect the confidentiality of the information they access during the audit, ensuring sensitive data remains secure and is only disclosed as necessary.

4. Professional Competence and Due Care: Auditors should possess the necessary skills, knowledge, and expertise to perform the audit effectively. They must exercise due professional care, applying diligence and diligence in their work.

5. Evidence-based Approach: Auditors rely on evidence to support their findings and conclusions. They collect and evaluate sufficient, appropriate, and reliable evidence to form an opinion on the subject matter under audit.

6. Independence: Auditors should be free from any conflicts of interest that could impair their judgment or objectivity. They must maintain independence from the entity being audited and any parties that may have a vested interest in the audit outcome.

7. Professional Behavior: Auditors should conduct themselves in a professional manner, adhering to ethical standards and codes of conduct. They should communicate effectively, document their work adequately, and respond appropriately to any conflicts or ethical dilemmas that may arise.

Or

(b) What is ‘Continuous Audit’? Discuss the limitations of Continuous Audit. Distinguish between Continuous Audit and Periodical Audit. 4+5+5=14

Ans: Continuous audit is a system of audit where the auditor and his staff Examines all the transactions and books of accounts in details continuously throughout the year at regular intervals i.e. weekly or fortnightly or monthly etc.

According to Spicer and Pegler, “a continuous audit is one where the auditor’s staff is occupied continuously on the accounts the whole year round, or where the auditor attends at intervals, fixed or otherwise, during the currency of the financial year and performs an interim audit; such audits are adopted where the work involved is considerable and have many points in their favour although they are subject to certain disadvantages.”

The following are the disadvantages of continuous audit:

(i) High Cost: As continuous audit is conducted throughout the year the organization has to give huge remuneration to the auditor. Therefore, a small concern cannot afford the high cost of conducting such audit.

(ii) Difficulties in accounting work: As a result of frequent visits of the auditor often it is seen that the books of accounts are checked by the audit staff and for this audit work is hampered.

(iii) Change of figures: It may so happen that the portion of accounts which have already examined by the auditor may alter the figures by the dishonest employees to achieve some personal interest.

(iv) Loss of continuity of work: As continuous audit is conducted at regular intervals, the auditor may left unchecked same audit work which was pending during his last audit work.

(v) Adverse effect on employee’s morale: Regular audit work can adversely affect the morale of the employee.

(vi) Monotony in Work: Continuous audit work can be monotonous and reduces the efficiency of employees.

(vii) Chances of collusion between organization’s staff and auditor’s staff: Continuous audit work affects the regular working of organisational staff and there is a chance of collusion between them and audit staff.

Difference between Continuous Audit and Periodical Audit:

4. (a) Discuss the duties of an auditor in connection with the vouching of credit purchases and purchase returns. 14

Ans: In auditing credit purchases and purchase returns, an auditor has several duties:

1. Verification of Documents: The auditor must verify invoices, purchase orders, delivery notes, and credit notes to ensure accuracy and authenticity.

2. Vouching: This involves tracing transactions from source documents to accounting records to ensure they are correctly recorded. For credit purchases, the auditor must verify that purchases were actually made and accurately recorded.

3. Examination of Internal Controls: The auditor assesses the effectiveness of internal controls related to credit purchases and purchase returns, such as approval processes, segregation of duties, and reconciliation procedures.

4. Review of Terms and Conditions: The auditor ensures that credit purchases adhere to agreed-upon terms and conditions, including payment terms, discounts, and return policies.

5. Evaluation of Allowances and Discounts: The auditor reviews allowances and discounts granted by suppliers to ensure they are properly authorized and accurately recorded.

6. Testing for Completeness and Accuracy: The auditor tests a sample of credit purchases and purchase returns to confirm that all transactions are recorded and accurately reflected in the financial statements.

7. Identification of Irregularities: The auditor looks for any irregularities or discrepancies in credit purchases and purchase returns, such as duplicate invoices, unauthorized purchases, or inflated returns.

8. Communication with Management: The auditor communicates any findings or concerns regarding credit purchases and purchase returns to management and provides recommendations for improvement if necessary.

Overall, the auditor's duties aim to ensure the reliability and accuracy of financial reporting related to credit purchases and purchase returns, safeguarding the interests of stakeholders.

Or

(b) Define vouching. What are the objectives of vouching? Distinguish clearly between the terms ‘Vouching’, ‘Verification’ and ‘Valuation’. 3+4+7=14

Ans: Vouching is the process of examining documentary evidence supporting transactions recorded in the accounting books to ensure their accuracy and authenticity. The objectives of vouching include verifying the existence, occurrence, completeness, accuracy, and proper authorization of transactions, as well as detecting and preventing errors and fraud.

The objectives of vouching:

1. Verification of Existence: Confirming that the transactions recorded in the accounting books actually occurred and are not fictitious.

2. Verification of Occurrence: Ensuring that the transactions occurred during the period under review and are not backdated or postdated.

3. Verification of Completeness: Checking that all relevant transactions have been recorded and none have been omitted.

4. Verification of Accuracy: Verifying the accuracy of the amounts recorded in the accounting books by cross-referencing them with supporting documents.

5. Verification of Proper Authorization: Ensuring that transactions were properly authorized according to established procedures and policies.

6. Detection of Errors: Identifying any errors in recording transactions, such as mathematical mistakes or misclassification.

7. Detection of Fraud: Identifying any fraudulent activities, such as misappropriation of assets, falsification of documents, or manipulation of financial records.

8. Prevention of Errors and Fraud: Implementing controls and measures to prevent future errors and fraud based on the findings of the vouching process.

Distinguish:

1. Vouching: It involves examining individual transactions to verify their authenticity and accuracy. Vouching aims to ensure that the recorded transactions have actually occurred and are properly supported by relevant documents and evidence.

2. Verification: Verification refers to the process of confirming the truth, accuracy, or validity of something. In the context of accounting, it typically involves verifying the existence, ownership, and valuation of assets and liabilities. Verification ensures that the financial statements present a true and fair view of the company's financial position.

3. Valuation: Valuation is the process of determining the monetary value of assets, liabilities, or businesses. It involves assessing various factors such as market conditions, future cash flows, and risk to arrive at a reasonable estimate of the worth of an asset or entity. Valuation is crucial for making informed investment decisions, financial reporting, and transactions such as mergers and acquisitions.

5. (a) How will you examine the following items while auditing the accounts of a limited company? 5+5+4=14

(1) Issue of Bonus Share.

(2) Redemption of Preference Share.

(3) Forfeiture of Share

Ans: How we can examine each of these items while auditing the accounts of a limited company:

1. Issue of Bonus Share:

- Review the board minutes to verify the authorization for issuing bonus shares.

- Examine the Articles of Association to ensure compliance with the company's regulations.

- Confirm that the bonus shares were issued out of the company's reserves.

- Verify the accuracy of the accounting treatment and disclosure in the financial statements.

2. Redemption of Preference Share:

- Inspect the terms of the preference shares to determine the redemption provisions.

- Review the board minutes for approval of the redemption and ascertain compliance with legal requirements.

- Confirm that the necessary funds were available for redemption and were utilized appropriately.

- Verify the accounting treatment of redemption premium, if any, and ensure proper disclosure in the financial statements.

3. Forfeiture of Share:

- Review the Articles of Association to understand the procedures for forfeiture.

- Examine board minutes to confirm that the forfeiture was properly authorized.

- Verify that the shareholder was given due notice and opportunity to rectify any default.

- Ensure compliance with legal requirements regarding the treatment of forfeited shares and disclosure in the financial statements..

Or

(b) (i) Explain the provisions of depreciation applicable to companies’ u/s 123(2) of Companies Act, 2013. 7

Ans:- The following are the explanation of the provisions of depreciation applicable to companies under Section 123(2) of the Companies Act, 2013:

Key Provisions:

1. Mandatory Depreciation: Companies are required to provide for depreciation on tangible assets, as per Section 123(2) of the Act. This means depreciation must be charged against profits before any dividend can be declared.

2. Schedule II: The basis for calculating depreciation is governed by Schedule II of the Act, which outlines:

- Useful Life: Specifies the expected useful life (in years) for various classes of assets (e.g., buildings, machinery, furniture).

- Residual Value: Sets a maximum residual value of 5% of the original cost of the asset.

3. Depreciation Methods: Companies have flexibility in choosing the depreciation method:

- Straight Line Method (SLM): Allocates a uniform amount of depreciation over the useful life.

- Written Down Value Method (WDV): Depreciation is calculated on the diminishing value of the asset each year.

4. Shift Working: Additional depreciation is allowed for assets used in multiple shifts:

- Double shifts: 50% increase in depreciation for that period.

- Triple shifts: 100% increase in depreciation for that period.

5. Exceptions to Schedule II: Companies can adopt a useful life or residual value different from Schedule II, provided they justify the reasons for such deviation.

6. Intangible Assets: Depreciation for intangible assets is not specifically addressed in Section 123(2) and Schedule II. It's generally governed by the applicable accounting standards.

7.Managerial Remuneration: Depreciation computed as per Section 123(2) is a mandatory deduction for determining the limits of managerial remuneration.

8. Non-Compliance: Failure to comply with depreciation provisions can result in penalties and potential litigation.

Additional Points:

- Depreciation is a non-cash expense that reflects the gradual wear and tear of assets over time.

- It helps companies accurately reflect the value of their assets in their financial statements.

- Companies should maintain proper records of assets and depreciation calculations to ensure compliance.

(ii) Discuss the duties of an auditor as regards provision for depreciation. 7

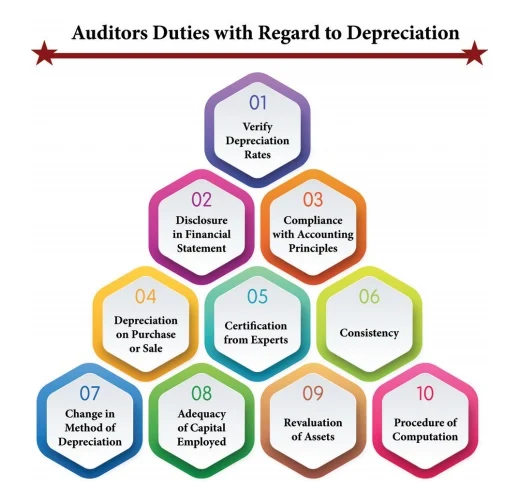

Ans:- An auditor is not a valuer to determine the value of assets held by the company. He has to depend on the suggestions and advice given by professional experts in determining the value and estimated life of the asset. However, the following are the duties of an auditor in this regard.

1. Verify Depreciation Rates: The auditor should ensure that depreciation has been provided as per the rates prescribed by the Companies Act.

2. Disclosure in Financial Statement: He should ascertain that adequate depreciation is charged and properly disclosed in the Profit and Loss Account and Balance Sheet.

3. Compliance with Accounting Principles: He should ensure that relevant accounting principles have been followed while providing for depreciation.

4. Depreciation on Purchase or Sale: When assets are purchased or sold during the year, auditor should ensure that depreciation is charged on pro-rata basis taking into account the date of purchase or sale and the accounting period.

5. Certification from Experts: In case the depreciation charged is more than the rates prescribed, he should examine whether same are based on professional and technical advice.

6. Consistency: Where difference rates are used for different assets, the same should be consistently applied over the years.

7. Change in Method of Depreciation: In case of a change in the method of accounting for depreciation it is recalculated from the date on which asset came into use and deficiency, if any, has been charged to Profit and Loss Account.

8. Adequacy of Capital Employed: Auditor should check whether the capital employed in the assets is being kept intact.

9. Revaluation of Assets: In case of revaluation of asset during the year he should ensure that depreciation is charged on revalued amounts.

10. Procedure of Computation: He should ensure that the procedure for calculating depreciation complies with the provisions of Companies Act and Income tax Act.

6. (a) What is Audit Report? Explain briefly about the various types of Audit Report. 4+10=14

Ans: An audit report is a formal document issued by an auditor after completing an audit engagement. It provides an independent assessment of an organization's financial statements, internal controls, or other aspects of its operations. The report communicates the auditor's findings, opinions, and recommendations to stakeholders, such as shareholders, regulators, and management.

There are several types of audit reports, each serving different purposes and conveying varying levels of assurance:

1. Unqualified Opinion: Also known as a clean opinion, this report indicates that the financial statements present a true and fair view in accordance with the applicable accounting standards. It's the most favorable type of report, indicating no material misstatements or issues.

2. Qualified Opinion: A qualified opinion is issued when the auditor believes that the financial statements are fairly presented overall, but there are certain limitations or departures from accounting principles. These issues are disclosed in the report.

3. Adverse Opinion: An adverse opinion is given when the auditor concludes that the financial statements do not present a true and fair view and are materially misstated. This is a serious finding and often indicates significant problems with the company's financial reporting.

4. Disclaimer of Opinion: When the auditor is unable to express an opinion due to significant limitations on the scope of the audit or insufficient evidence, they issue a disclaimer of opinion. This might occur if the auditor cannot obtain enough information or encounters conflicts of interest.

5. Other Reports: In addition to the above, auditors may issue reports on specific aspects of a company's operations, such as internal controls or compliance with regulations. These reports provide valuable insights into specific areas of concern or improvement opportunities.

Or

(b) Discuss the elements and features of a good Audit Report. 7+7=14

Ans: A good audit report should possess several key elements and features to effectively communicate the auditor's findings and provide value to stakeholders:

1. Clarity and Conciseness: The report should be written in clear and straightforward language, avoiding technical jargon whenever possible. It should be concise, focusing on the most significant findings and recommendations.

2. Comprehensive Coverage: The report should cover all relevant aspects of the audit engagement, including the scope of work, methodology used, key findings, and conclusions reached. It should address both positive aspects and areas needing improvement.

3. Objectivity and Independence: The report should maintain the auditor's objectivity and independence throughout, presenting findings impartially and without bias. It should be free from any undue influence or conflicts of interest.

4. Compliance with Standards: A good audit report should adhere to applicable auditing standards and regulatory requirements. This ensures consistency and reliability in the audit process and enhances the credibility of the report.

5. Identification of Risks and Issues: The report should clearly identify any significant risks or issues discovered during the audit, including potential implications for the organization. It should provide sufficient detail for stakeholders to understand the nature and severity of these risks.

6. Transparency and Disclosure: Transparency is essential in an audit report. It should disclose any limitations or constraints encountered during the audit process, as well as the basis for the auditor's conclusions and opinions. This transparency enhances the credibility and trustworthiness of the report.

7. Actionable Recommendations: A good audit report should include actionable recommendations for addressing identified weaknesses or areas for improvement. These recommendations should be practical, feasible, and aimed at enhancing the organization's operations and financial reporting processes.

Overall, a well-written audit report should provide stakeholders with a clear understanding of the organization's financial health, internal controls, and compliance with regulations, while also offering insights and recommendations for improvement.

-000000-

We hope you find the above solutions helpful for your exam preparation. If you liked them, please do share this post with your friends. Once again, if you find any mistakes or have any suggestions, feel free to comment below or email us. We will be happy to hear from you and make the necessary corrections. Your feedback means a lot to us!

![Auditing Solved Question Paper 2023 [Dibrugarh University BCom 6th Semester]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjQB6Whgd-k11pOx4CaoSjAQXWPVCZMwqiOniD3mu2DlmfhO_OU7MBZ-07UV_2lfB-cX05thmiJQzXduq3g1kOm42Qm2N4a-mM2fC9ihP4WBxRFQKaoD7_w-dhq0U4DpgguB_V91IAE8jCfEYnMBN1TMoCdgwZv7CgEobDbVUPJbKjAS4yABxtubrFcMyLC/w200-h200-p-k-no-nu/Dibrugarh%20auditing%20solve%20question%20paper%202023.jpg)