![Banking Solved Question Paper 2023 PDF [Gauahti University B.Com 5th Sem]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjOIZK36WvCv39WAEEgN4v1eTHHXp4NSiBOMo5FuAd2zYfs9Yz_rhW2OTSRCkxRpgCTBNzo-0qZaiyc2-w8jyG-BDYcCQQWjevyoHUIBcQGzCrBJWZtUGJuGbczy3jHcKtuSKllBYEyaxtnxqRnBgbWCx7UBmqZFtjqqlJQUEspV7AMF7hlGYf1Rrk1X8Ls/s990/Banking%20Solved%20paper%202023%20Gauhati%20university%20bcom%20hons.webp "Banking Solved Question Paper 2023 PDF [Gauahti University B.Com 5th Sem]")

In this post we have Shared Gauhati University Banking Solved Question Paper Solution 2023 Pdf, B.Com 5th Sem GU Paper Solution, Which can be very beneficial for your upcoming exam preparation. So read this post from top to bottom and get familiar with the question paper solution .

Banking Solved Question Paper 2023

[Gauhati University B.Com 5th Sem CBCS]

4(Sem-5/CBCS) COM HE4(BNK)

2023

COMMERCE

(Honours Elective)

Paper: COM-HE-5046

(Banking)

Full Marks : 80

Time: Three hours

The figures in the margin indicate full marks for the questions.

1.(A) Choose the most appropriate answer son to the following questions: 1 x 5 = 5

(a) In which year Regional Rural Bank Act was passed?

(i) 1934

(ii) 1955

(ii) 1969

(iv) 1976

Ans:- iv) 1976

(b) Who issues the Garnishee Order ?

(i) Court

(ii) RBI

(iii) The Central Government

(iv) Concerned State Government

Ans:- I) Court

(c) Which of the following is not a liquid asset?

(i) Cash

(ii) Money at call

(iii) Bond

(iv) Share

Ans:- iii) Bond

(d) Which of the following is a party to a Bill of Exchange?

(i) Drawer

(ii) Drawee

(iii) Payee

(iv) All of the above

Ans:- iv) All of the above

(e) The Provisions of the Banking Regulation Act, 1949 are not applicable in case of-

(i) SBI

(ii) Nationalised Banks

(iii) Private Sector Banks

(iv) None of the above

Ans:- (iv) None of the above

(B) State whether the following statements are true or false : 1 x 5 = 5

(a) The issuing bank grants loan for every Transaction settled through credit card.

Ans:- False.

(b) The Integrated Ombudsman Scheme was introduced in the year 2021.

Ans:- True.

(c) A married woman is considered as a special type of bank customer.

Ans:- False.

(d) Crossing of a cheque is an example of material alteration.

Ans:- False.

(e) There are three parties in a promissory note.

Ans:- False.

2. Give brief answer to the following questions : 2 x 5 = 10

(a) Define 'Bank'.

Ans:- A bank is a financial institution that accepts deposits from the public, provides loans, and offers various financial services such as saving accounts, credit facilities, and payment processing. Banks play a crucial role in the economy by facilitating financial transactions, promoting savings, and providing funds for investment.

(b) Write the meaning of the term 'Bank Customer'.

Ans:- A bank customer is an individual or entity that holds an account with a bank and uses its financial services. The relationship between a bank and its customer is typically established through an account, and the customer may avail various services like deposits, loans, and payment transfers.

(c) What is meant by the term 'Liquidity of Assets'?

Ans:- Liquidity of assets refers to the ease with which an asset can be quickly converted into cash without significantly losing its value. Liquid assets include cash, marketable securities, and other instruments that can be easily sold or redeemed in the financial markets.

(d) Write the meaning of the term 'endorsement' in the context of a negotiable instrument.

Ans:- Endorsement in the context of a negotiable instrument refers to the act of signing the back of the instrument (such as a cheque or bill of exchange) by the holder to transfer the rights or ownership of the instrument to another person or entity. This makes the new holder eligible to receive the payment or value.

(e) Classify the assets of a bank as per the guidelines of RBI.

Ans:- As per RBI guidelines, the assets of a bank are classified into the following categories:

- Standard Assets: Performing assets that generate regular income for the bank.

- Sub-standard Assets: Assets that have been classified as non-performing for less than 12 months.

- Doubtful Assets: Assets that have been non-performing for more than 12 months but have a chance of recovery.

- Loss Assets: Assets that are considered irrecoverable by the bank, though some value may be recoverable.

3. Answer the following questions in about 200 words each : (any four) 5x4 = 20

(a) Write a short note on the powers of the RBI under the Banking Regulation Act, 1949.

Ans:- Write a short note on the powers of the RBI under the Banking Regulation Act, 1949.

The Banking Regulation Act, 1949 grants the Reserve Bank of India (RBI) extensive powers to regulate and oversee the banking sector in India. Some of the key powers of the RBI under the Act include:

- Licensing of Banks: The RBI has the authority to issue and revoke banking licenses, ensuring only qualified institutions operate as banks.

- Regulation of Shareholding: RBI monitors and controls the shareholding and voting rights in banks, ensuring compliance with legal limits.

- Capital and Reserve Requirements: RBI sets the minimum capital and reserve requirements that banks must maintain for financial stability.

- Supervision and Inspection: The RBI conducts regular inspections of banks to ensure compliance with regulatory standards and can take corrective actions if any deficiencies are found.

- Control over Management: The RBI can approve or remove directors and key managerial personnel in banks, ensuring that qualified individuals manage the institutions.

- Interest Rate Control: RBI has the authority to regulate the rates of interest that banks can charge on loans and offer on deposits.

- Merger and Reconstruction: The RBI can approve the merger of banks or direct restructuring to safeguard the interests of depositors and maintain financial stability.

(b) What are the different methods available for fund transfer under E-Banking system ? Explain.

Ans:- What are the different methods available for fund transfer under E-Banking system? Explain.

E-Banking provides several convenient methods for transferring funds electronically. The most commonly used methods include:

1. NEFT (National Electronic Funds Transfer):

NEFT allows the transfer of funds from one bank account to another within India. It operates in hourly batches and is widely used for small to medium-sized transactions. NEFT is a secure and reliable system for both individual and business transactions.

2. RTGS (Real-Time Gross Settlement):

RTGS is a real-time fund transfer system that enables the transfer of large amounts of money. Unlike NEFT, RTGS processes transactions individually and in real-time. It is typically used for high-value transactions, where immediacy is crucial.

3. IMPS (Immediate Payment Service):

IMPS is a real-time instant payment system that operates 24/7, allowing users to transfer funds at any time. IMPS is available for small-value transactions and provides immediate confirmation of the transfer, making it popular for mobile and online banking.

4. UPI (Unified Payments Interface):

UPI is a mobile-based real-time payment system that allows users to link multiple bank accounts to a single mobile application and make instant payments. It is user-friendly and facilitates peer-to-peer fund transfers as well as payments to merchants.

5. ECS (Electronic Clearing Service):

ECS is mainly used for bulk transfers like salary disbursements, utility bill payments, or loan installments. It operates on a scheduled date and enables the automatic transfer of funds from one account to multiple accounts or vice versa.

6. Cards (Credit/Debit Cards):

Credit and debit cards allow the transfer of funds for purchases or payments electronically through point-of-sale (POS) terminals or online platforms. They are widely accepted for both domestic and international transactions.

(c) What are the different types of account facilities available in a commercial bank?

Ans:- Commercial banks offer various types of accounts to meet the diverse financial needs of their customers. These include:

1. Savings Account:

A savings account is a deposit account that offers interest on the balance while providing easy access to funds. It is suitable for individuals looking to save money while maintaining liquidity. Withdrawals are subject to certain limitations, but it provides a safe place to save with moderate interest.

2. Current Account:

A current account is primarily designed for businesses, firms, and professionals who conduct frequent banking transactions. It typically does not offer interest but allows unlimited withdrawals and deposits, making it ideal for daily transactions.

3. Fixed Deposit Account (FD):

A fixed deposit account allows customers to deposit a lump sum for a specified tenure at a fixed interest rate. The funds cannot be withdrawn before the maturity date without penalties. FDs offer higher interest rates compared to savings accounts, making them suitable for long-term savings.

4. Recurring Deposit Account (RD):

In a recurring deposit account, the customer deposits a fixed amount at regular intervals (usually monthly) over a predetermined period. At the end of the term, the customer receives the total deposited amount along with the accrued interest. RDs are useful for disciplined savings over time.

5. Demat Account:

A Demat (Dematerialized) account is used to hold shares and securities in electronic form. It is essential for investors in the stock market as it allows the buying, selling, and holding of shares without the need for physical share certificates.

6. NRI Accounts:

Banks also offer specific accounts for Non-Resident Indians (NRIs), such as NRE (Non-Resident External), NRO (Non-Resident Ordinary), and FCNR (Foreign Currency Non-Resident) accounts, which facilitate transactions and savings in foreign or Indian currencies for individuals living abroad.

(d) Explain briefly about the different types of credit facilities provided by a commercial bank.

Ans:- Commercial banks provide a wide range of credit facilities to meet the diverse financing needs of individuals, businesses, and corporations. These include:

1. Term Loans:

Term loans are provided for a fixed period, typically for a specific purpose like purchasing equipment, expanding business, or personal needs like home loans or education loans. The borrower repays the loan in installments over the tenure of the loan, which can range from a few months to several years.

2. Overdraft Facility:

An overdraft facility allows account holders to withdraw more money than they have in their accounts, up to a pre-approved limit. The bank charges interest only on the overdrawn amount, and this facility is particularly useful for businesses to manage short-term cash flow gaps.

3. Cash Credit (CC):

Cash credit is a short-term loan provided to businesses for working capital requirements. The borrower can withdraw funds up to a certain limit based on the value of their inventory or receivables. Interest is charged only on the utilized amount. It provides flexibility in managing day-to-day business needs.

4. Letter of Credit (LC):

A letter of credit is a financial instrument issued by a bank on behalf of a buyer, guaranteeing payment to the seller upon fulfilling certain conditions. It is commonly used in international trade transactions to mitigate payment risks between buyers and sellers.

5. Bank Guarantee (BG):

A bank guarantee is a commitment by the bank to pay a specified amount to a third party if the borrower fails to fulfill their contractual obligations. It acts as a risk mitigation tool in business transactions, ensuring that the obligations will be met.

6. Working Capital Loans:

These loans are provided to businesses to cover their daily operational expenses such as payroll, rent, and utility bills. They are usually short-term loans aimed at helping businesses manage liquidity and maintain smooth operations.

7. Personal Loans:

Personal loans are unsecured loans provided to individuals for personal needs like medical expenses, travel, or weddings. The borrower is not required to provide any collateral, and the loan is repaid in fixed installments over time.

8. Credit Cards:

Credit cards provide a revolving line of credit to cardholders, allowing them to make purchases or withdraw cash up to a credit limit. The borrower is expected to repay the borrowed amount within a certain period, with interest charged on outstanding balances.

9. Housing Loans:

Banks offer housing loans to individuals for purchasing, constructing, or renovating residential property. These loans are typically long-term, and the property itself serves as collateral.

10. Vehicle Loans:

Vehicle loans are provided for purchasing cars, motorcycles, or commercial vehicles. The bank holds the ownership of the vehicle as collateral until the loan is fully repaid.

(e) Discuss the basic features of a cheque.

Ans:- cheque is a negotiable instrument used for transferring money from one person or entity to another. The basic features of a cheque include:

1. Instrument in Writing:

A cheque must be in writing, either handwritten or printed, and signed by the drawer (the person issuing the cheque).

2. Unconditional Order:

A cheque represents an unconditional order to the bank to pay the specified amount to the payee or the bearer of the cheque.

3. Parties Involved:

There are three parties in a cheque:

- Drawer: The person who writes the cheque and instructs the bank to make the payment.

- Drawee: The bank that is directed to make the payment.

- Payee: The person or entity to whom the payment is to be made.

4. Payable on Demand:

A cheque is payable on demand, meaning the bank must pay the amount immediately upon presentation.

5. Specified Amount:

The cheque must clearly specify the amount to be paid, written both in words and numbers, to avoid any ambiguity.

6. Date:

A cheque must be dated, and the date should not be post-dated or more than three months old, as it becomes invalid after the expiration of this period.

7. Signature of Drawer:

The cheque must bear the signature of the drawer to validate it. Without the signature, the cheque is not legally enforceable.

8. Crossing:

A cheque can be crossed, either generally or specially. A crossed cheque can only be deposited into a bank account and cannot be encashed directly. This enhances security.

9. Bank Account Linkage:

The cheque is linked to the drawer’s bank account, and the bank will only honor it if the account has sufficient funds to cover the amount.

(f) Explain the structure of commercial banks in India.

Ans:- The structure of commercial banks in India is organized into several tiers, based on ownership, operations, and regulatory framework. The key components of this structure include:

1. Public Sector Banks:

These are banks in which the majority stake (51% or more) is owned by the Government of India. Public sector banks play a dominant role in the Indian banking system due to their extensive network and large customer base. They are classified into two categories:

- Nationalized Banks: These banks were originally private banks but were nationalized by the government to promote financial inclusion. Examples include Punjab National Bank, Bank of Baroda, and Canara Bank.

- State Bank of India (SBI) and its Associates: SBI is the largest public sector bank in India, and it previously had several associate banks that were merged into SBI in 2017.

2. Private Sector Banks:

These banks are owned and operated by private individuals or institutions. They are regulated by the RBI but operate with a higher degree of autonomy compared to public sector banks. Private sector banks are known for offering innovative services and greater efficiency. Examples include HDFC Bank, ICICI Bank, and Axis Bank. Private banks are further classified into:

- Old Private Sector Banks: These were established before 1969 and were not nationalized. They include banks like City Union Bank and Catholic Syrian Bank.

- New Private Sector Banks: These were established after the liberalization of the banking sector in the 1990s. Examples include Kotak Mahindra Bank and Yes Bank.

3. Foreign Banks:

Foreign banks operate in India as branches of international banks. They offer banking services to both domestic and international customers and are typically involved in corporate banking and international trade financing. Examples include Citibank, Standard Chartered Bank, and HSBC.

4. Regional Rural Banks (RRBs):

RRBs were established to provide banking services in rural areas, especially to small farmers, artisans, and agricultural laborers. They are jointly owned by the Government of India, the respective state government, and a sponsoring public sector bank. RRBs focus on providing credit and financial services to the rural population and promoting financial inclusion.

5. Cooperative Banks:

Cooperative banks are structured as cooperatives and cater to the financial needs of specific communities or groups, such as farmers, small businesses, and individuals in rural areas. They operate at both urban and rural levels:

- Urban Cooperative Banks: Focus on serving the urban population, offering services similar to commercial banks.

- Rural Cooperative Banks: Operate mainly in rural areas, providing agricultural credit and financial services to farmers.

6. Payment Banks:

Payment banks are a recent addition to the banking structure in India. These banks are allowed to accept deposits up to a certain limit (currently ₹2 lakh) and provide payment and remittance services. However, they are not allowed to lend money or issue credit cards. Examples include Paytm Payments Bank and Airtel Payments Bank.

7. Small Finance Banks (SFBs):

Small finance banks are specialized banks aimed at serving the unbanked and underserved sections of society, including small businesses, marginal farmers, and micro-entrepreneurs. They can accept deposits and provide loans, focusing primarily on financial inclusion. Examples include Ujjivan Small Finance Bank and Equitas Small Finance Bank.

4.Answer the following questions in about 600 words each : (any four). 10×4=40

(a) Elaborately discuss the major developments in the Indian banking sector during the post-Independence period.

Ans:- The Indian banking sector has undergone significant transformations since Independence, shaped by various policy measures, reforms, and technological advancements. The major developments can be grouped into different phases:

1. Nationalization of Banks (1969 & 1980):

One of the most significant milestones in the Indian banking sector was the nationalization of 14 major private banks in 1969, followed by the nationalization of 6 more banks in 1980. This move was aimed at making banking services accessible to the broader population, especially in rural areas, and ensuring that credit was available for priority sectors like agriculture, small-scale industries, and export.

2. Formation of Regional Rural Banks (1975):

To further extend banking facilities to the rural population, Regional Rural Banks (RRBs) were established in 1975. RRBs were set up with the aim of providing credit to small farmers, artisans, and agricultural laborers. RRBs functioned as a hybrid between cooperatives and commercial banks, with financial support from the government, state governments, and public sector banks.

3. Liberalization and Banking Sector Reforms (1991):

The liberalization of the Indian economy in 1991 brought about major reforms in the banking sector. The recommendations of the Narasimham Committee laid the foundation for:

- Entry of Private Banks: The Indian banking sector was opened to private players, leading to the emergence of new private sector banks such as ICICI Bank, HDFC Bank, and Axis Bank. These banks brought in modern technology, better customer service, and innovative financial products.

- Reduction of Statutory Pre-emptions: The Statutory Liquidity Ratio (SLR) and Cash Reserve Ratio (CRR) were progressively reduced, allowing banks to lend more freely and improve their profitability.

- Greater Autonomy for Public Sector Banks: Public sector banks were given more operational freedom, including the ability to raise capital from the market.

4. Technological Advancements:

Post-liberalization, Indian banks started adopting new technologies, leading to automation and digitalization:

- Introduction of ATMs: The introduction of Automated Teller Machines (ATMs) revolutionized banking services by providing 24/7 access to cash and basic banking functions.

- Core Banking Solutions (CBS): Banks moved towards CBS, which centralized their operations and made it easier for customers to access their accounts from any branch.

- Internet and Mobile Banking: The early 2000s saw the rapid growth of internet banking and, later, mobile banking. These services enabled customers to perform banking transactions remotely without visiting branches.

5. Financial Inclusion Initiatives:

The Indian government and the Reserve Bank of India (RBI) have launched several programs to promote financial inclusion:

- Pradhan Mantri Jan Dhan Yojana (PMJDY): Launched in 2014, PMJDY aimed at providing every household access to a bank account and affordable financial services. Millions of zero-balance bank accounts were opened under this scheme, promoting formal banking in rural and underserved areas.

- Direct Benefit Transfer (DBT): To ensure that government subsidies and benefits reach the intended beneficiaries, the DBT scheme was implemented through bank accounts. This reduced leakage and corruption.

6. Demonetization and Push Towards a Cashless Economy (2016):

The demonetization of ₹500 and ₹1,000 notes in 2016 was a landmark event that accelerated the adoption of digital banking and cashless transactions. The government promoted the use of digital wallets, UPI (Unified Payments Interface), and card payments, transforming the payment landscape in India.

7. Introduction of Payment Banks and Small Finance Banks (2015):

To further enhance financial inclusion, RBI introduced payment banks and small finance banks. Payment banks, such as Paytm Payments Bank and Airtel Payments Bank, focus on providing basic banking services like savings accounts and remittance services. Small finance banks, such as Ujjivan Small Finance Bank, focus on lending to underserved sectors like micro, small, and medium enterprises (MSMEs), farmers, and small entrepreneurs.

8. Bank Consolidation (2017 onwards):

In recent years, the Indian banking sector has seen significant consolidation, particularly in public sector banks. The government merged several public sector banks to create stronger and more resilient institutions capable of competing on a global scale. For example, in 2019, Bank of Baroda was merged with Dena Bank and Vijaya Bank, while in 2020, 10 public sector banks were merged into 4 larger banks.

9. Development of Fintech and UPI:

The rise of fintech companies has transformed the banking ecosystem in India, with digital payment platforms such as Paytm, PhonePe, and Google Pay becoming household names. The Unified Payments Interface (UPI), launched by NPCI in 2016, became a game-changer by enabling instant money transfers using mobile devices. UPI has become one of the most popular modes of payment in India, facilitating billions of transactions monthly.

Or

(b) Do you think that providing banking services in electronic mode is advantageous for both the banker and customer? Justify your answer.

Ans:- Yes, providing banking services in electronic mode is advantageous for both bankers and customers. Here's why:

Advantages for the Banker:

1. Cost Efficiency:

Electronic banking reduces the need for physical infrastructure such as branches and staff, which in turn lowers operational costs for banks. With online services, banks can handle a larger volume of transactions without significant increases in costs.

2. Increased Reach:

E-banking allows banks to reach customers in remote areas without having to establish physical branches. This promotes financial inclusion and expands the bank's customer base.

3. Enhanced Productivity:

Digital banking automates various processes like fund transfers, bill payments, and account management, which streamlines operations and reduces human error. This allows bank employees to focus on more value-added services, improving overall productivity.

4. Customer Retention and Satisfaction:

Providing convenient electronic services like mobile banking, internet banking, and digital payments improves the customer experience, increasing customer loyalty and retention. Offering seamless services helps banks remain competitive in the market.

5. Data Collection and Analytics:

Electronic banking enables banks to collect vast amounts of customer data, which can be analyzed to gain insights into customer behavior, preferences, and spending patterns. This helps banks personalize their offerings and develop targeted marketing strategies.

Advantages for the Customer:

1. Convenience:

E-banking allows customers to access banking services anytime and from anywhere, eliminating the need to visit a physical branch. This saves time and effort for customers, making banking more convenient.

2. 24/7 Availability:

Unlike traditional banking, which operates during specific hours, electronic banking services are available 24/7. Customers can perform transactions, pay bills, and check their accounts at any time, even on holidays.

3. Faster Transactions:

Digital banking significantly speeds up transactions, especially for fund transfers, bill payments, and loan applications. Real-time payment systems like UPI and IMPS provide instant money transfers, improving the overall banking experience.

4. Access to a Wide Range of Services:

Through electronic banking platforms, customers can easily access a variety of services, such as managing multiple accounts, applying for loans, investing in financial products, and paying utility bills, all from the convenience of their smartphones or computers.

5. Enhanced Security:

Modern e-banking platforms are equipped with advanced security measures, such as two-factor authentication, encryption, and biometric verification, which enhance the safety of customer transactions. While there are risks of cyber fraud, banks continue to strengthen their security frameworks to protect customers.

6. Cost Savings:

Customers can save on travel and other costs associated with visiting bank branches. Additionally, e-banking often comes with lower service charges for activities like bill payments or fund transfers compared to traditional banking.

(c) Discuss the obligations of the banker towards his customer in the context of

(i) Honouring customers' cheque and

(ii) Maintaining secrecy of customers' account. 5 + 5 = 10

Ans:-

(i) Honouring Customers' Cheques

One of the fundamental duties of a banker towards its customers is to honor their cheques when presented for payment, provided certain conditions are met. This obligation is governed by banking laws and practices. The banker is obligated to honor the cheque under the following conditions:

1. Sufficient Funds:

The bank must honor a cheque if the customer's account has sufficient funds to cover the amount mentioned in the cheque. If the balance is insufficient, the bank can refuse to honor the cheque and may return it with a "Cheque Dishonored" note.

2. Properly Drawn Cheque:

The cheque must be properly filled out with no discrepancies. It must be signed by the account holder (the drawer) and the details (payee, amount, date) must be clearly specified. Any material alteration (like changing the amount or date) without proper authentication by the drawer can lead to the cheque being dishonored.

3. Cheque Presented Within Validity:

The cheque should be presented to the bank within its validity period, typically three months from the date of issue. If presented after the validity period, the bank has the right to reject the payment.

4. No Legal Prohibition:

If there are any legal instructions, such as a garnishee order or a court injunction, which prohibits the payment from the customer’s account, the bank is not obligated to honor the cheque.

5. Genuine Cheque:

The bank must ensure that the cheque is genuine and not forged. If a bank pays out on a forged cheque, it may be held liable to the customer for any resulting losses. The bank should exercise due diligence to detect forgeries.

6. No Stop Payment Instructions:

If the customer has issued a "stop payment" instruction for a cheque, the bank is obliged to follow the instruction and not honor the cheque, even if there are sufficient funds in the account.

Consequences of Dishonoring a Valid Cheque:

- If the bank refuses to honor a cheque that meets all the required conditions (sufficient funds, proper signature, no legal restrictions, etc.), it may be liable for damages to the customer for breach of contract.

- The customer may sue the bank for wrongful dishonor of cheques, especially if the dishonor causes reputational or financial loss.

(ii) Maintaining Secrecy of Customers' Accounts

Another critical obligation of a banker is maintaining the confidentiality or secrecy of the customer's account details. This duty is both ethical and legal, aimed at ensuring that the financial dealings of the customer remain private. The key points related to maintaining secrecy include:

1. Non-Disclosure to Third Parties:

The bank must not disclose any information about a customer's account, including account balance, transactions, or personal details, to any third party without the explicit consent of the customer. This includes family members, business partners, or other unauthorized entities.

2. Banker-Customer Confidentiality:

This obligation arises from the contractual relationship between the bank and the customer. The bank is legally bound to keep all information related to the customer’s account confidential as part of their fiduciary duty. This confidentiality extends beyond the customer's active banking relationship, even after the account is closed.

3. Exceptions to Confidentiality:

There are certain circumstances under which the bank can disclose information about the customer’s account:

- With Customer's Consent: If the customer explicitly authorizes the bank to share information with third parties, such as in the case of loan applications or reference checks.

- Legal Obligation: If the bank is required to disclose information under a court order, income tax laws, or other regulatory authorities, it is obligated to comply with such orders.

- Public Duty: The bank may also disclose information if it is in the public interest, such as cases involving fraudulent activities or money laundering.

- Bank’s Own Interest: If the bank needs to disclose customer information to protect its own interests, for example, in the event of a dispute regarding loan recovery, it may do so within legal boundaries.

4. Consequences of Breach of Secrecy:

- Legal Liability: If a bank unlawfully discloses a customer’s confidential information without authorization, it can face legal action from the customer for breach of confidentiality. The customer may sue for damages or compensation for any financial or reputational harm caused by the disclosure.

- Loss of Trust: Maintaining confidentiality is essential for the trust between a bank and its customers. Any breach of this trust can lead to the loss of business and damage to the bank's reputation.

5. Banking Codes and Standards:

The Indian banking sector follows the Code of Bank’s Commitment to Customers, which lays down the principles of fairness and transparency in dealing with customer information. Banks are expected to follow these codes to ensure the safety of customer data and maintain privacy.

OR

(d) What is meant by Crossing of Cheque ? Explain briefly about the different types of crossing with their specimen.2 + 8 = 10

Ans:- Crossing of a cheque refers to drawing two parallel lines on the face of the cheque, with or without additional words between them. This crossing is a direction to the bank that the cheque must be deposited directly into a bank account and not encashed over the counter. The purpose of crossing is to add an extra layer of security, ensuring that the amount is transferred only to a person having a bank account.

Definition: Crossing of a cheque is nothing but instructing the banker to pay the specified sum through the banker only, i.e. the amount on the cheque has to be deposited directly to the bank account of the payee.

There are several types of crossing

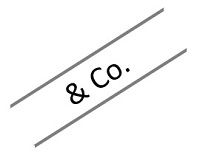

General Crossing: When across the face of a cheque two transverse parallel lines are drawn at the top left corner, along with the words & Co., between the two lines, with or without using the words not negotiable. When a cheque is crossed in this way, it is called a general crossing.

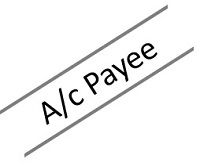

Restrictive Crossing: When in between the two transverse parallel lines, the words ‘A/c payee’ is written across the face of the cheque, then such a crossing is called restrictive crossing or account payee crossing. In this case, the cheque can be credited to the account of the stated person only, making it a non-negotiable instrument.

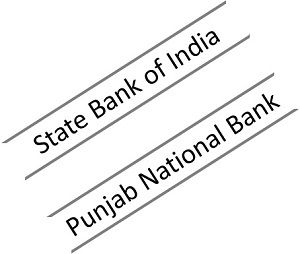

Special Crossing: A cheque in which the name of the banker is written, across the face of the cheque in between the two transverse parallel lines, with or without using the word ‘not negotiable’. This type of crossing is called a special crossing. In a special crossing, the paying banker will pay the sum only to the banker whose name is stated in the cheque or to his agent. Hence, the cheque will be honoured only when the bank mentioned in the crossing orders the same.

Not Negotiable Crossing: When the words not negotiable is mentioned in between the two transverse parallel lines, indicating that the cheque can be transferred but the transferee will not be able to have a better title to the cheque.

Double Crossing: Double crossing is when a bank to whom the cheque crossed specially, further submits the same to another bank, for the purpose of collection as its agent, in this situation the second crossing should indicate that it is serving as an agent of the prior banker, to whom the cheque was specially crossed.

The crossing of a cheque is done to ensure the safety of payment. It is a well-known mechanism used to protect the parties to the cheque, by making sure that the payment is made to the right payee. Hence, it reduces fraud and wrong payments, as well as it protects the instrument from getting stolen or encashed by any unscrupulous individual.

(e) Differentiate between 'Holder' and 'Holder in Due Course'. Also explain the privileges enjoyed by the Holder in Due Course.

4 + 6 = 10

Ans:- Difference Between 'Holder' and 'Holder in Due Course'

Privileges of Holder in Due Course

Better Title: A holder in due course holds the cheque free from all prior defects of title. If the previous holder had a defective title, the holder in due course can still claim the amount.

Right Against Prior Parties: The holder in due course has the right to sue all prior parties to the cheque or bill of exchange. Every party involved in the transaction is liable to the holder in due course.

Protection Against Fraud: If the instrument was originally obtained through fraud, but later came into the possession of a holder in due course, the holder is protected from such claims, provided they were unaware of the fraud.

Right to Immediate Payment: The holder in due course has the right to demand immediate payment without any disputes related to previous endorsements or transactions.

No Effect of Conditional Delivery: Even if the cheque was delivered conditionally (subject to certain conditions between previous parties), a holder in due course can claim payment regardless of such conditions.

Defenses Against Dishonored Cheques: The holder in due course has stronger defenses in case the cheque is dishonored (not paid) by the drawer.

OR

Discuss the provisions of the Banking Regulation Act, 1949 in regard to

(i) Licensing of banks

(ii) Constitution of the Board of Directors 5 + 5 = 10

Ans:- The Banking Regulation Act, 1949 is a key legislation in India that governs the regulation and supervision of commercial banks. It empowers the Reserve Bank of India (RBI) to regulate banks and ensure sound banking practices. Let’s discuss the provisions under this Act regarding the licensing of banks and the constitution of the board of directors.

(i) Licensing of Banks (Section 22 of the Banking Regulation Act, 1949)

The licensing of banks is one of the key provisions under the Banking Regulation Act. No banking company can commence or carry on banking business without a license from the Reserve Bank of India (RBI). The provisions regarding the licensing of banks include the following:

1. Requirement of License:

- Every banking company in India must obtain a license from the RBI before starting its business. This applies to new banks as well as existing ones.

2. Conditions for Granting License:

- The RBI grants a license only if it is satisfied that the bank has adequate capital structure, earnings prospects, and management.

- The RBI also considers whether the public interest will be served by granting the license.

3. Application for License:

- The application for a banking license must contain details about the bank’s capital structure, management, and business plan, among other things.

4. Cancellation of License:

- The RBI has the authority to cancel the license of any bank if the bank does not comply with the conditions set forth by the RBI, or if its affairs are being conducted in a manner detrimental to depositors or public interest.

5. Regulation of Foreign Banks:

- Foreign banks that wish to establish a branch or commence business in India also require a license from the RBI. The same conditions apply to them as for domestic banks.

6. Inspection of Banks:

- The RBI has the power to inspect the books of accounts and other records of a bank at any time before granting a license or after issuing it, to ensure compliance with the prescribed conditions.

(ii) Constitution of the Board of Directors (Section 10B of the Banking Regulation Act, 1949)

The constitution of the Board of Directors in a banking company is also regulated by the Act. Key provisions include:

1. Minimum Number of Directors:

- Every banking company must have a board of directors consisting of at least five directors. A chairman must be appointed to preside over the board meetings and handle specific functions.

2. Fit and Proper Criteria:

- The Act mandates that directors must possess adequate professional qualifications or experience in banking, economics, finance, law, or business management.

- The RBI has the authority to scrutinize the qualifications and expertise of individuals who are appointed to the board of a bank to ensure they meet the "fit and proper" criteria.

3. Appointment of Whole-time Chairman:

- If the office of the chairman is held by a whole-time director, the appointment must be made with the prior approval of the RBI.

- A whole-time chairman or managing director must be appointed for a term not exceeding five years at a time, subject to RBI approval for reappointment.

4. Restrictions on Directorship:

- A director of a banking company cannot be a director of more than one company, excluding subsidiaries and other specified exceptions. This is to prevent conflict of interest and ensure that directors can focus on their responsibilities to the bank.

- The Act also disqualifies certain individuals, such as those who have been adjudicated as insolvent or convicted of offenses involving moral turpitude, from becoming directors.

5. Removal of Directors:

- The RBI has the power to remove any director from the board of a bank if it believes that their continuation in office is prejudicial to the interests of depositors or the bank's sound functioning.

6. Representation of Employees:

- In public sector banks, provisions exist for the representation of employees on the board, in accordance with the guidelines issued by the government and RBI. This helps maintain transparency and inclusivity in governance.

Conclusion

The provisions of the Banking Regulation Act, 1949, regarding the licensing of banks ensure that only well-capitalized and well-managed entities can enter the banking sector, with oversight from the RBI. Meanwhile, the constitution of the board of directors provisions ensure that qualified and responsible individuals manage the bank, which safeguards the interests of depositors and ensures the smooth functioning of the bank.

(g) Discuss the procedure of opening savings bank account in 'ONLINE' and 'OFFLINE' mode.

Ans:- Procedure for Opening a Savings Bank Account

Opening a savings bank account can be done through ONLINE and OFFLINE modes, each with its own set of procedures. Here’s a detailed overview of both methods:

1. ONLINE Mode

The process of opening a savings bank account online typically involves the following steps:

1. Visit the Bank's Website or Mobile App:

- Navigate to the official website of the bank or download its mobile application.

2. Select 'Open Account' Option:

- Look for the option that says "Open Savings Account" or similar. Click on it to initiate the process.

3. Fill Out the Application Form:

- Complete the online application form with personal details such as name, date of birth, contact information, address, and other relevant information.

4. Upload Documents:

- Upload the necessary documents as specified by the bank, which usually include:

- Identity Proof (Aadhar card, passport, voter ID, etc.)

- Address Proof (utility bill, rental agreement, etc.)

- Photographs (passport-sized photographs).

- Income Proof (if required, based on bank policies).

5. Complete KYC Process:

- Most banks require Know Your Customer (KYC) verification. This can sometimes be done through video KYC, where a bank official verifies your identity through a video call.

6. Set Up Online Banking:

- During the application process, you may be asked to create online banking credentials (username and password) for easy access to your account.

7. Review and Submit Application:

- Review all the details provided and submit the application. You may receive an acknowledgment via email or SMS confirming the submission.

8. Account Activation:

- After verification of documents and KYC, the bank will activate your account. You will receive your account number and other details through email or SMS. A debit card may also be issued, which will be sent to your registered address.

2. OFFLINE Mode

Opening a savings bank account offline involves the following steps:

1. Visit the Bank Branch:

- Go to the nearest branch of the bank where you wish to open an account.

2. Request an Application Form:

- Ask for a savings account application form from the bank officials. You can also download the form from the bank's website and fill it out beforehand.

3. Fill Out the Application Form:

- Provide accurate information in the application form, including your personal details, occupation, and contact information.

4. Submit Required Documents:

- Attach photocopies of the required documents (identity proof, address proof, photographs, etc.) to the application form. The bank may also ask to see the originals for verification.

5. KYC Process:

- The bank will conduct the KYC process at the branch. This might involve filling out a KYC form and providing additional information as needed.

6. Initial Deposit:

- Depending on the bank's policy, you may need to make an initial deposit to activate your account. This can be done in cash or via cheque.

7. Review and Sign:

- Review the terms and conditions provided by the bank. Sign the required forms and agreements.

8. Account Activation:

- After processing your application, the bank will open your account and provide you with your account number. You may receive your debit card and other account-related materials by mail or in person.

OR

(h) Discuss the principles of sound lending followed by a commercial bank.

Ans:- Principles of Sound Lending Followed by a Commercial Bank

Commercial banks follow several key principles of sound lending to ensure that they make prudent lending decisions while managing risks effectively. These principles include:

1. Safety:

- The primary principle of lending is to ensure the safety of funds. Banks must evaluate the creditworthiness of borrowers to minimize the risk of default. Proper risk assessment helps ensure that loans are granted to borrowers who are capable of repaying them.

2. Liquidity:

- Banks must maintain sufficient liquidity to meet withdrawal demands from depositors. When lending, banks should ensure that the loan repayment schedules align with their liquidity requirements. Loans should ideally have a clear repayment schedule that does not compromise the bank's liquidity.

3. Profitability:

- Banks need to ensure that lending is profitable. They assess the interest rate that borrowers are willing to pay and the associated risks. The bank must ensure that the interest earned on loans exceeds the cost of funds and operational costs.

4. Purpose of Loan:

- The purpose for which the loan is being taken is crucial. Banks must assess whether the loan will be used for productive purposes that can generate income for the borrower, ensuring that they can repay the loan.

5. Repayment Capacity:

- Banks should thoroughly evaluate the borrower's repayment capacity, including their income, cash flows, and existing obligations. This assessment helps ensure that the borrower can meet the repayment obligations without financial strain.

6. Creditworthiness:

- The credit history of the borrower plays a significant role in the lending process. Banks conduct background checks and evaluate the borrower's credit score, past repayment behavior, and overall financial health.

7. Diversification:

- To minimize risk, banks should diversify their loan portfolios. By lending to different sectors, industries, and borrowers, banks can mitigate the impact of defaults in any specific area.

8. Legal Compliance:

- Lending practices must comply with relevant laws and regulations. Banks should ensure that all lending processes adhere to legal requirements, including documentation and terms of the loan agreements.

9. Monitoring:

- Once a loan is disbursed, banks should regularly monitor the borrower’s financial condition and the project funded by the loan. This ongoing monitoring helps identify potential repayment issues early, allowing the bank to take corrective actions if necessary.

10. Documentation:

- Proper documentation is essential for sound lending. Banks should maintain detailed records of loan agreements, collateral, and all correspondence with the borrower. This ensures transparency and accountability.

-00000-

![Banking Solved Question Paper 2023 PDF [Gauahti University B.Com 5th Sem]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjOIZK36WvCv39WAEEgN4v1eTHHXp4NSiBOMo5FuAd2zYfs9Yz_rhW2OTSRCkxRpgCTBNzo-0qZaiyc2-w8jyG-BDYcCQQWjevyoHUIBcQGzCrBJWZtUGJuGbczy3jHcKtuSKllBYEyaxtnxqRnBgbWCx7UBmqZFtjqqlJQUEspV7AMF7hlGYf1Rrk1X8Ls/w200-h200-p-k-no-nu/Banking%20Solved%20paper%202023%20Gauhati%20university%20bcom%20hons.webp)